Existing Client? Login

Article

Self-funded vs. Fully Insured

Group medical benefit plans typically fall into one of two categories: self-funded or fully insured. The choice of one over the other should not be made arbitrarily. Each type carries its own set of administrative rules and legal constraints.

What is Self-funding?

Under an insured health benefit plan, an insurance company assumes the financial and legal risk of loss in exchange for a fixed premium paid to the carrier by the employer. Employers with self-funded (or self-insured) plans retain the risk of paying for their employees’ health care themselves, either from a trust or directly from corporate funds.

Most employers with more than 200 employees self-insure some or all of their employee health benefits. Many employers with fewer than 200 employees also self-fund, but these employers require greater stop-loss insurance protection than larger employers (stop-loss insurance is discussed in greater detail later). As a general rule, employers with fewer than 100 employees fully insure their group medical benefits.

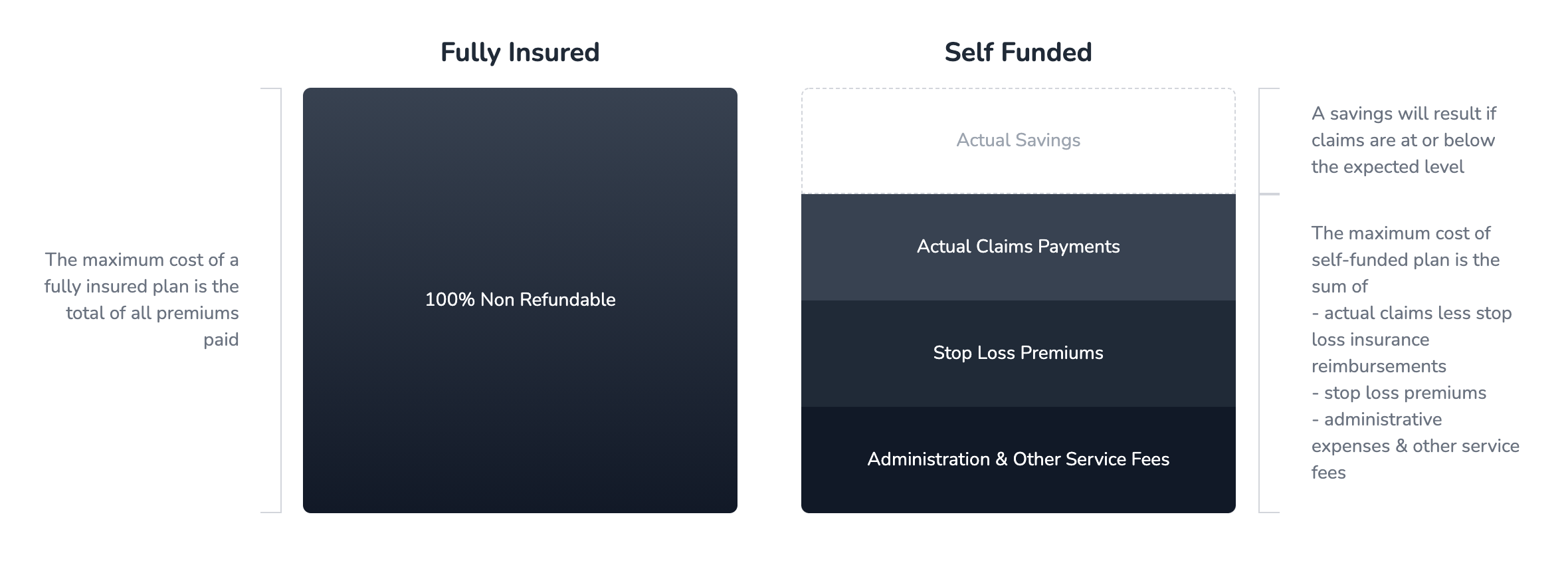

The risk assumed in either situation is the chance that employees will become ill and require costly treatment. When employees have few claims and few expensive illnesses, the self-funded employer realizes an immediate positive impact on overall health care costs. Conversely, if the employee group has unfavorable claims experience, a self- funded employer would incur an immediate expense beyond what may have been expected. Insured plans have a more predictable cost for the year; however, large employee claims costs from one year can affect future premium amounts.

ERISA vs. State Regulation

Self-funded health plans are governed by the Employee Retirement Income Security Act of 1974 (ERISA). ERISA preempts state insurance regulations, meaning that employers with self-funded medical benefits are not required to comply with state insurance laws that apply to medical benefit plan administrators. On the other hand, insured plans must comply with some of ERISA’s requirements, but are primarily governed by the state where covered employees reside.

The distinction between state and ERISA regulations is important when determining if self-funding is right for your organization. Multi-state companies with insured health plans must comply with the regulations of each state in which they have plans and covered employees. Multi-state self-funded plans need only comply with ERISA.

Premium vs. Unbundled Fees

The risk an insurance company takes with an insured plan can be translated into a dollar amount for the employer. That dollar amount is the premium an employer pays each month for the insured group medical benefits. The premium amount includes the following:

- Current and predicted claims cost

- Administrative fee

- Premium tax paid to the state

- Insurance company profit

Employers who self-fund their medical benefits do not pay the premium tax or insurance company profit. They do, however, assume the costs of paying for claims and administrative functions. Typically, employers with self- funded health plans will outsource plan administration to a third-party administrator (TPA) or insurance company who charges the employer a fee for performing administrative services.

Stop-loss Insurance

Employers with self-funded health plans typically carry stop- loss insurance to reduce the risk associated with large individual claims or high claims from the entire plan. The employer self-insures up to the stop-loss attachment point, which is the dollar amount above which the stop-loss carrier will reimburse claims. Stop-loss insurance comes in two forms: individual/specific stop-loss and aggregate stop-loss.

Individual/Specific Stop-loss Insurance

This protects a self-funded employer against large individual health care claims. Essentially, it limits the amount that the employer must pay for each individual. For example, an employer with a specific stop-loss attachment point of $25,000 would be responsible for the first $25,000 in claims for each individual plan participant each year. The stop-loss carrier would pay any claims exceeding $25,000 in a calendar year for a particular participant.

Aggregate Stop-loss Insurance

This protects the employer against high total claims for the health care plan. For example, aggregate stop-loss insurance with an attachment point of $500,000 would begin paying for claims after the plan’s overall claims exceeded $500,000. Any amounts paid by a specific stop-loss policy for the same plan would not count toward the aggregate attachment point

Nondiscrimination Rules

Nondiscrimination rules require employers to offer employee benefits that do not favor certain employees. Employers with insured plans do not have nondiscrimination rules for group medical benefits, provided they follow the policy requirements of the sponsoring insurance carrier. However, employers with self-funded plans are required to comply with nondiscrimination rules. Generally these requirements are not difficult to meet, but failure to comply can result in some employees having their benefits treated as taxable income.

Employers with either type of group medical plan are required to comply with certain reporting and disclosure requirements, usually by providing tax and other pertinent documents to the United States Department of Labor or to their particular state.

Typically self-funded plans are required to provide copies of plan communications such as summary plan descriptions (SPDs) and summary of material modifications if the plan language changes.

Employers with insured plans that require employee contributions must file certain financial documents with the IRS. IRS filings are also required of self-funded plans, including Form 5500 and any accompanying documents.

Marty Thomas

Marty has spent most of the last 20 years developing software in the marketing space and creating pathways for software systems to talk to each other with high efficiency. He heads our digital marketing efforts as well as oversees any technology implementations for our clients. As a partner, Marty is also responsible for internal systems in which help our team communicates with each other and our clients.